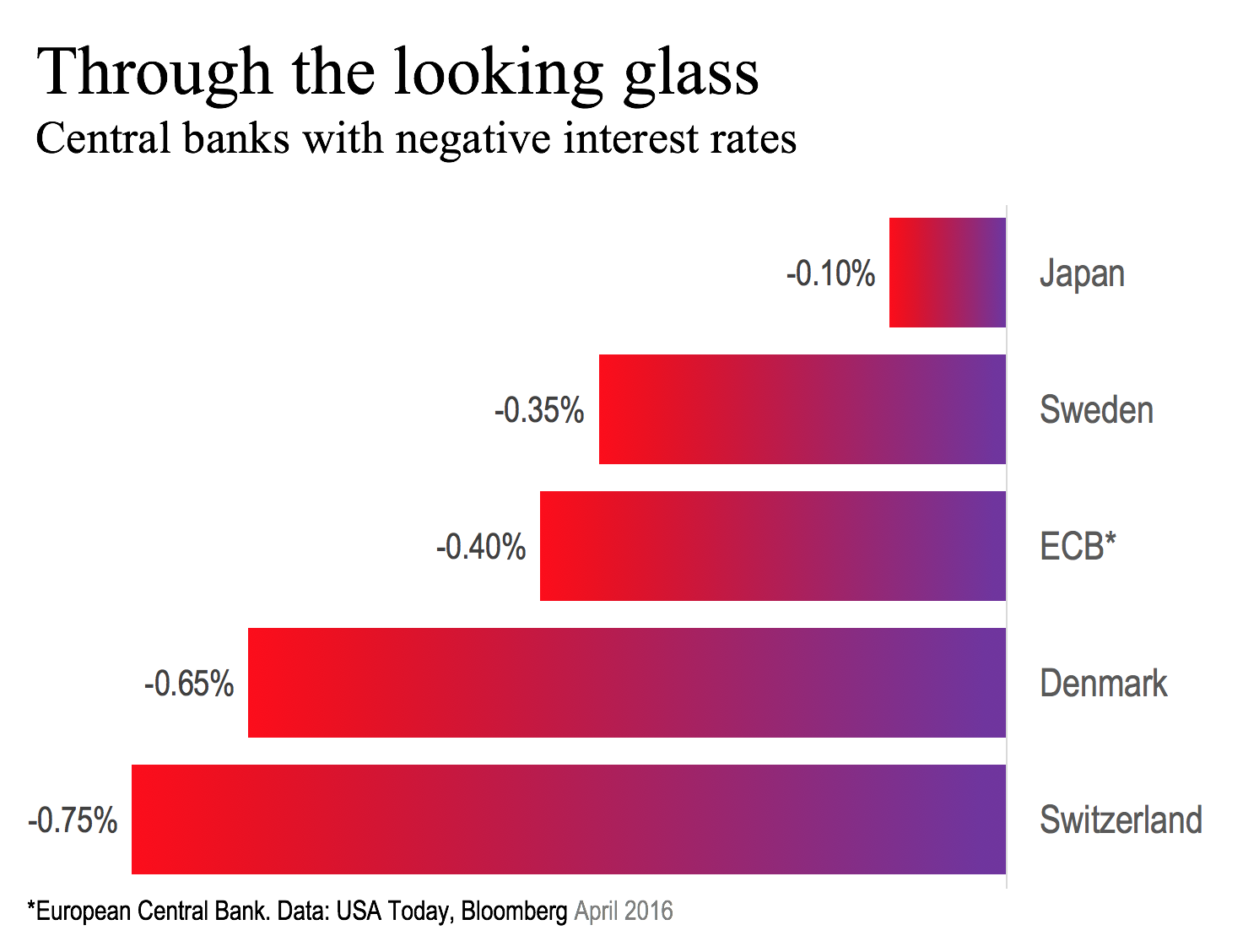

What if the negative interest rate policies (NIRP) that have been adopted by major central banks had effects opposite what was intended?

What if the negative interest rate policies (NIRP) that have been adopted by major central banks had effects opposite what was intended?

The idea is to fight DEflation and to nudge consumers to spend by penalizing banks for keeping money on deposit.

The theory is that banks will lend rather than take a haircut, and that those who’ve borrowed money will spend it. Weak demand is one of the principal reasons that the global economy remains in a funk.

The theory sounds plausible enough. But in fact, low interest rates in the long run incentivize consumers to save rather than spend. Larry Fink, CEO of Blackrock, the universe’s largest asset manager with $4.7 trillion under its wing, makes this case in his annual letter to shareholders.

People need to invest more today to achieve their desired annual retirement income… For example, a 35-year-old looking to generate $48,000 per year in retirement income beginning at age 65 would need to invest $178,000 today in a 5% interest rate environment. In a 2% interest rate environment, however, that individual would need to invest $563,000 (or 3.2 times as much) to achieve the same outcome in retirement. This reality has profound implications for economic growth: consumers saving for retirement need to reduce spending if they are going to reach their retirement income goals and retirees with lower incomes will need to cut consumption as well. A monetary policy intended to spark growth, then, in fact, risks reducing consumer spending.

Economists at the International Monetary Fund argue that the benefits of this unprecedented NIRP experiment outweigh the costs. But they also argue that there are limits to to both how far and for how long NIRP can go. A more balanced fight against deflation and weak demand would include structural reforms and supportive fiscal policies.

As the IMF economists point out, low interest rates in general and NIRP in particular have other real-world consequences, intended or otherwise. Bankers, who live and die by net interest margin, the difference between what they pay for deposits and what they can get on loans, find their profits squeezed. Bankers may be tempted to take greater risks to offset this squeeze.

Low rates risk inflating asset prices, contributing to booms, which inevitably are followed by busts. A house in my modest middle-class neighborhood just sold for more than $1 million. I doubt the price would have been nearly so high had the mortgage rate been 5-6% rather than the likely 3-4%. The Fed’s near-zero interest-rate policy (N-ZIRP) is arguably the main reason stock-market values have run up so much over the past six years. Low rates have benefited mainly the rich rather than the middle class.

And negative rates may in time lead to hoarding of and even shortages of high-denomination bank notes. Why not keep your savings in $100 bills or 500 Euro notes are even 1,000 Swiss franc notes if your bank is going to charge you for the privilege of keeping money on deposit. That’s not yet happened yet at the consumer level in advanced economies, but don’t think it is not possible if U.S. nominal rates stay super low or dip into negative territory.

Partly as the result of negative rates, Japanese are hoarding cash. The Wall Street Journal reports that sales of home safes have skyrocketed. Japan’s Finance Ministry is stepping up production of the largest-denomination currency in Japan.

A Journal editorial concluded that “Japan’s experience is the ultimate cautionary tale of what happens when leaders rely on monetary policy and government spending to goose an overregulated and overtaxed economy.” Sound familiar?